On July 21, 2026, the strongest legal tool women had for challenging lending discrimination stops existing under federal law. The CFPB’s final Regulation B rule eliminates disparate impact liability from the Equal Credit Opportunity Act. That means proving a lender’s policies systematically deny women at higher rates is no longer enough. You now have to prove they intended to discriminate.

That’s not a nuance. That’s a different legal universe.

But here’s what most coverage is missing: the federal government was never the only game in town. Some states built their own fair lending walls — thick ones. Others built nothing and relied entirely on federal law. After July 21, the difference between those two categories is the difference between having a legal remedy and having a strongly worded letter.

This is your state-by-state map. Bookmark it. You’re going to need it.

What Disappears on July 21, 2026

Before diving into what your state does or doesn’t offer, you need to understand exactly what’s being taken off the table at the federal level. Read the full Regulation B disparate impact countdown for the complete picture.

Disparate Impact Liability Under ECOA: Gone

What it was: Disparate impact let you challenge lending policies that were neutral on paper but discriminatory in outcome. A bank’s collateral policy that happened to exclude the asset types women-owned businesses hold most often? Challengeable. A credit scoring model that penalized employment gaps from parental leave? Challengeable. You didn’t need to find a smoking gun memo. You needed data.

What it did: It was the only realistic enforcement mechanism for the kind of discrimination that actually exists in 2026 — algorithmic, structural, built into policy rather than spoken aloud. According to the Husch Blackwell analysis, removing this standard means creditors can maintain policies with demonstrably discriminatory outcomes as long as no intentional bias is proven.

What replaces it: Disparate treatment — intentional discrimination. You now need to prove the lender deliberately targeted you because of your gender. In practice, this means internal communications, admission of bias, or pattern evidence so overwhelming a court can infer intent. For a small business owner without subpoena power, that bar is functionally unreachable.

SPCP Restrictions: Closing the Door on Women-Specific Programs

Simultaneously, the same rule tightens conditions on Special Purpose Credit Programs — the legal mechanism that allowed lenders to create targeted lending programs for women. Read about SPCP restrictions and women-specific lending programs to understand the full scope. Programs that specifically served women borrowers are either restructuring or shutting down.

The tools that let institutions voluntarily fix the lending gap are disappearing alongside the tools that let you legally challenge it. Both exits closing at once is not a coincidence. It’s a policy architecture.

The Discouragement Standard: Narrowed

The Cooley analysis highlights another significant change: the discouragement standard — which prohibited lenders from discouraging people from applying — has been narrowed to require that discouragement be based on a protected class characteristic. A loan officer steering you toward a smaller, more expensive product without referencing your gender directly? That’s no longer covered.

The Federal Protections That Remain

Not everything is gone. But what remains is either narrower than most people realize or further away than most people can wait.

Fair Housing Act Disparate Impact: Mortgage Only

The Fair Housing Act still recognizes disparate impact claims — but only for housing-related lending. If you’re applying for a mortgage, you retain the right to challenge discriminatory outcomes without proving intent. If you’re applying for a business line of credit, an equipment loan, or an SBA loan, the Fair Housing Act doesn’t apply. Period.

ECOA Intentional Discrimination: Still Prohibited, Rarely Provable

The Equal Credit Opportunity Act still prohibits intentional discrimination. A lender cannot say “we don’t lend to women” and claim legal protection. But as the Venable analysis notes, the practical barrier to proving intentional discrimination without disparate impact analysis is enormous. You need evidence of intent — and modern lending discrimination doesn’t announce itself.

Section 1071 Data: Coming 2028 (Maybe)

The revised Section 1071 rule requires lenders to begin collecting small business lending data — including demographic information — but the effective date is now 2028. And the rule was gutted from 81 data points to 13, covering approximately 280 lenders instead of the original 2,500. When the data finally arrives, it will be too thin to detect the patterns that disparate impact analysis would have caught.

FTC Unfairness Authority: Still Alive, Rarely Used

The Federal Trade Commission retains authority to pursue “unfair or deceptive acts or practices.” This is a real enforcement tool — but the FTC has historically prioritized consumer protection over business lending enforcement, and its current bandwidth is stretched thin. Don’t build your strategy around an agency that has never made women’s business lending a priority.

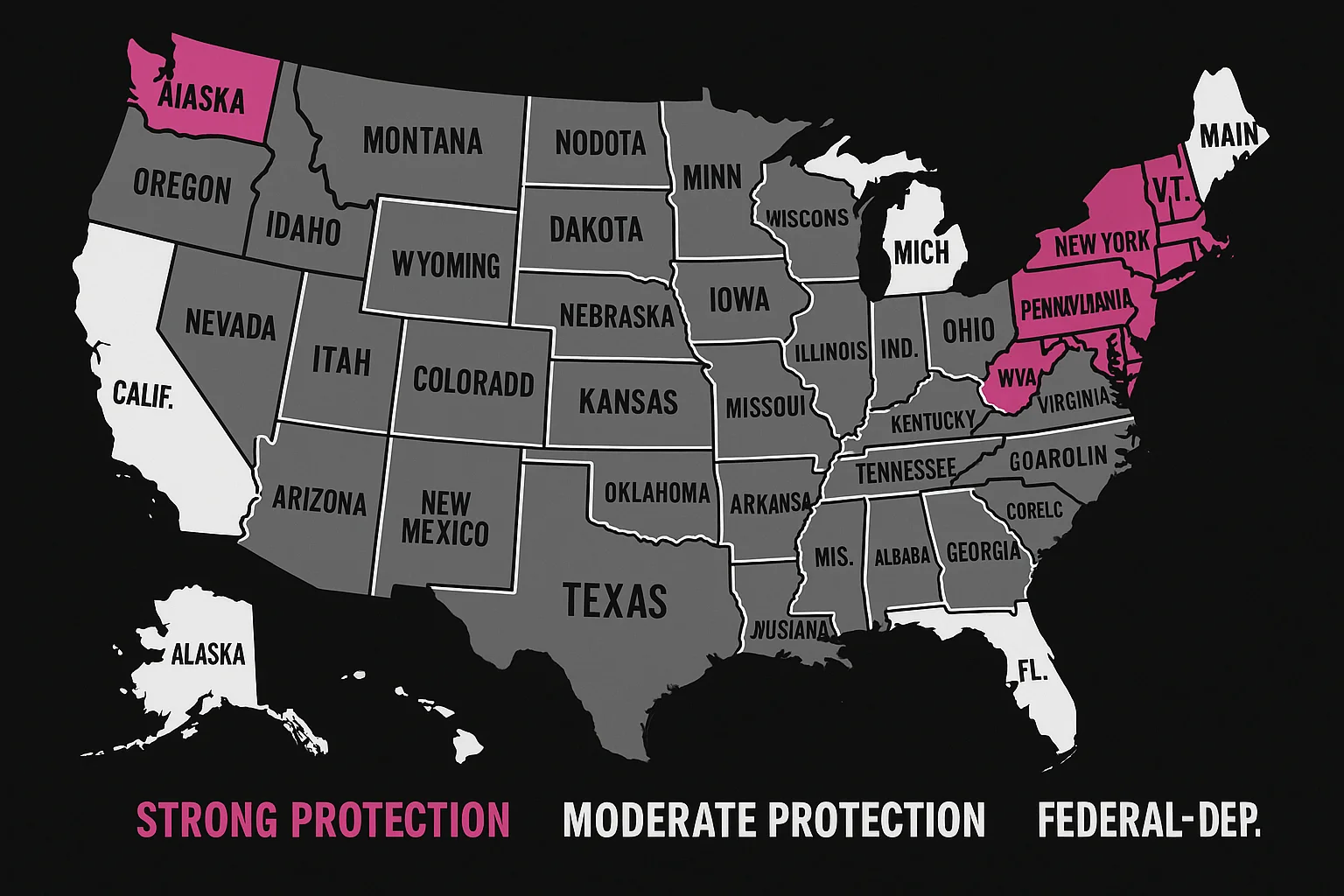

The States With Their Own Armor

Here’s where your zip code starts to matter more than your federal rights. Some states anticipated the federal retreat and built independent protections. Others relied on Washington entirely. After July 21, the difference is stark.

Tier 1: Strong Independent Protection

These states have fair lending statutes, active enforcement mechanisms, and — critically — independent authority to pursue lending discrimination without relying on federal disparate impact doctrine.

New York

Key law: New York Human Rights Law (Executive Law Section 296-a)

New York’s Human Rights Law explicitly covers credit transactions and recognizes disparate impact as an independent basis for claims — entirely separate from federal ECOA. This means the July 21 rule change has zero effect on your rights under New York law if your lending transaction touches New York.

The state also enacted the FAIR Act in early 2026, extending “unfair, deceptive, and abusive” protections to business borrowers for the first time. AG Letitia James has been aggressively building cases against predatory business lenders.

What you can do: File complaints with the New York Division of Human Rights or the AG’s office. Both have independent investigative authority and don’t need CFPB referrals to act.

California

Key laws: Unruh Civil Rights Act + California Fair Lending Act + DFPI Enforcement

California runs a triple-layer defense. The Unruh Civil Rights Act provides broad anti-discrimination protection in all business establishments — including banks. The California Fair Lending Act requires state-level data reporting that the gutted federal 1071 rule no longer mandates. And the Department of Financial Protection and Innovation (DFPI) functions as a state-level CFPB with real investigative teeth.

California’s data reporting requirements mean discriminatory patterns are still detectable even after the federal data infrastructure collapses. And the DFPI is actively investigating lending discrimination complaints — not just collecting them.

What you can do: File fair lending complaints with the DFPI. If you were denied by a California-regulated lender, request your lending data under state law. Document everything.

Massachusetts

Key law: Chapter 151B (Anti-Discrimination Statute)

Massachusetts Chapter 151B covers credit transactions and the state’s AG office has been one of the most active in the country on consumer and business lending enforcement. The Massachusetts Commission Against Discrimination (MCAD) accepts and investigates lending discrimination complaints independently.

AG Andrea Campbell has made predatory lending a stated enforcement priority, with particular attention to disparate outcomes in small business lending.

What you can do: File with the MCAD or the AG’s Consumer Protection Division. Massachusetts has a private right of action — meaning you can sue under state law, not just file a complaint and wait.

Illinois

Key law: Illinois Human Rights Act (775 ILCS 5/)

Illinois explicitly covers credit transactions under its Human Rights Act and maintains independent disparate impact analysis authority through the Illinois Department of Human Rights. The state also expanded its Community Reinvestment Act authority in 2025, requiring state-chartered banks to report lending data that the federal government no longer demands.

What you can do: File with the Illinois Department of Human Rights. The statute carries a private right of action with potential compensatory damages, attorney’s fees, and injunctive relief.

Washington State

Key law: Washington Law Against Discrimination (RCW 49.60)

Washington’s Law Against Discrimination is one of the broadest civil rights statutes in the country. It covers credit transactions, recognizes disparate impact claims, and is enforced by the Washington State Human Rights Commission. The state AG’s office has an active Consumer Protection Division with standalone authority to investigate lending practices.

What you can do: File with the Washington State Human Rights Commission or the AG’s Consumer Protection Division. Washington courts have a strong track record of recognizing disparate impact in credit transactions.

Tier 2: Moderate Protection

These states have fair lending statutes that offer meaningful protection — but with narrower scope, less aggressive enforcement, or gaps that limit their practical value.

New Jersey

New Jersey codified disparate impact under state law and added algorithmic transparency requirements for AI-powered lending decisions. If an algorithm rejects your application, the lender must explain why in human terms. Strong on paper. Enforcement is ramping up but not yet at Tier 1 levels.

Key limitation: Coverage gaps for certain types of commercial financing, including some MCA products.

Connecticut

Connecticut’s fair lending protections cover credit transactions, and the state Department of Banking has investigative authority. The AG’s office has pursued lending discrimination cases, though less frequently than Tier 1 states.

Key limitation: Fewer resources dedicated to business lending specifically. Most enforcement activity centers on consumer mortgage lending.

Oregon

Oregon’s Unlawful Discrimination in Credit Transactions statute (ORS 659A.421) prohibits discrimination in credit and has been interpreted to cover business lending. The state Bureau of Labor and Industries handles complaints.

Key limitation: Limited precedent for business lending disparate impact claims. Most case law involves consumer credit.

Minnesota

Minnesota Human Rights Act covers credit transactions and the state Department of Human Rights processes complaints. The AG’s office has been active on consumer protection but less focused on business lending discrimination specifically.

Key limitation: Business lending complaints are accepted but have historically received less attention than consumer lending complaints.

Colorado

Colorado’s Anti-Discrimination Act covers credit and the state Civil Rights Division investigates complaints. Colorado also requires commercial financing cost disclosures — including APR-equivalent calculations for MCAs — giving borrowers more transparency than most states.

Key limitation: Commercial financing disclosure requirements are strong, but the discrimination enforcement apparatus is thinner than Tier 1 states.

Tier 3: Federal-Dependent States

These states relied primarily on federal law for lending discrimination protection. After July 21, their residents face the weakest protections in the country.

States in this category include: Texas, Florida, Georgia, Ohio, Tennessee, Alabama, Mississippi, Louisiana, South Carolina, North Carolina, Arizona, Indiana, Missouri, Kentucky, Oklahoma, Arkansas, Kansas, Nebraska, South Dakota, North Dakota, Wyoming, Idaho, Montana, and West Virginia.

That’s not a complete list. It’s a representative one. And it covers roughly half the US population.

What these states typically lack:

- No state-level disparate impact standard for credit transactions

- No independent state fair lending enforcement beyond federal referrals

- No state-level data reporting requirements for business lending demographics

- Limited AG enforcement — UDAP statutes exist but are rarely applied to lending discrimination

- No private right of action under state law for credit discrimination

If you’re a woman business owner in a Tier 3 state, your lending discrimination protections after July 21 consist of: (1) the right to file a federal disparate treatment complaint you’ll struggle to prove, (2) the right to file an FTC complaint about general unfairness, and (3) the right to hire a lawyer. That’s it.

State AG Enforcement: The New Front Line

Even in states without dedicated fair lending statutes, your state Attorney General may still be your best remaining option. Here’s why — and how to use them.

The UDAP Backstop

Every state has some form of Unfair or Deceptive Acts and Practices (UDAP) statute. While these weren’t designed specifically for lending discrimination, they can cover predatory lending practices. An AG who interprets “unfair” broadly has meaningful authority to investigate lenders, issue subpoenas, and bring enforcement actions.

The catch: “can” and “will” are different words. AG enforcement is discretionary. Your complaint matters more if it fits an AG’s existing priorities.

The Active Enforcement States

State AGs who have made lending discrimination or predatory business lending an explicit enforcement priority:

- New York — AG Letitia James. Active FAIR Act enforcement. Dedicated business lending unit.

- California — AG Rob Bonta. Active coordination with DFPI on fair lending. Pursuing MCA providers.

- Massachusetts — AG Andrea Campbell. Stated predatory lending priority. Active consumer protection division.

- Illinois — AG Kwame Raoul. Active enforcement of Illinois Human Rights Act in credit contexts.

- Washington — AG Bob Ferguson. Consumer Protection Division pursuing lending cases.

- New Jersey — AG Matt Platkin. Algorithmic transparency enforcement ramping up.

- Minnesota — AG Keith Ellison. Active consumer protection but limited business lending focus.

- Pennsylvania — AG Michelle Henry. Consumer protection focus expanding toward small business lending.

- Oregon — AG Ellen Rosenblum. Consumer protection activity with some business lending overlap.

How to File a State AG Complaint

- Locate your AG’s consumer protection portal. Search “[Your State] Attorney General consumer complaint.”

- Frame the complaint as a pattern. AGs prioritize systemic behavior. If you know other women denied by the same lender under similar circumstances, include it.

- Include specific data. Denial dates, amounts, reasons given, comparable approvals if known. Concrete evidence gets flagged for investigation.

- Reference the applicable state statute. Cite the specific fair lending or UDAP law. This signals you know your rights.

- File with multiple entities. State AG, state banking department, CFPB, and FTC — simultaneously. Redundancy is protection.

Multi-State AG Coalitions

When AGs from multiple states jointly investigate a lender, the enforcement weight approximates what the CFPB has abandoned. In 2025–2026, AG coalitions have targeted predatory MCA providers, fintech lenders with unexplained algorithmic rejections, and national banks applying different underwriting standards by region. It’s slower than federal action. But it’s real.

What to Do Before July 21: A State-by-State Checklist

You have weeks, not months. Here’s your action plan.

Step 1: Identify Your State’s Tier

Use the state lists above. If your state isn’t named, search “[Your State] fair lending statute credit” and “[Your State] disparate impact credit discrimination.” If you find a specific statute covering credit transactions with independent enforcement, you’re in Tier 2 at minimum. If your search returns only federal references, you’re in Tier 3.

Know this number: Your state tier determines your fallback strategy for every lending interaction from July 21 forward.

Step 2: Bookmark Your Complaint Portals

Don’t wait until you need them. Bookmark these now:

- Your state AG’s consumer/business complaint form — search “[State] Attorney General complaint”

- Your state banking department complaint form — search “[State] Department of Banking” or “Division of Financial Regulation”

- Your state human rights commission (if applicable) — for states with fair lending under civil rights statutes

- CFPB complaint portal — consumerfinance.gov/complaint (still active, still creates a record even if enforcement is weak)

- HUD Fair Housing complaint — hud.gov/fair_housing (for mortgage-related discrimination only)

- FTC complaint — reportfraud.ftc.gov

Step 3: Consider Banking Relationships in Stronger States

This is a legitimate strategy, not a loophole. Banks chartered in Tier 1 states often apply their home state’s higher compliance standards nationally. It’s operationally easier than maintaining two compliance systems.

- A bank headquartered in New York may apply FAIR Act-level lending practices even when serving customers in Texas.

- An online lender regulated by the California DFPI operates under California’s fair lending framework regardless of where you’re located.

- National banks with significant California or New York operations often default to the stricter standard.

This doesn’t guarantee protection. But it increases the probability that the institution you’re borrowing from operates under tighter rules than your state requires.

When evaluating lenders across regulatory environments, tools like Lendesca can help you compare lending options and identify institutions with stronger compliance frameworks — particularly useful if you’re in a Tier 3 state looking for lenders that voluntarily maintain higher standards.

Step 4: Document Your Current Lending Relationships

Before July 21, create a record of your existing lending terms, approval history, and bank relationships. This documentation serves two purposes:

- Baseline evidence. If your lending terms change after July 21 — higher rates, reduced credit lines, new requirements — the before-and-after documentation strengthens any future complaint.

- Pattern detection. If you apply for refinancing or new credit after July 21 and get denied under different criteria than your original approval, you have contemporaneous evidence of the shift.

Document these specifically:

- Current loan terms, rates, and conditions

- Most recent credit line review and any communications about your account

- Names and dates of every lending interaction in the past 12 months

- Any denial letters or adverse action notices — save these permanently

- Screenshots of your online banking portal showing current terms (terms can change; screenshots can’t)

Step 5: Know Your Remaining Federal Options

Even after July 21, you retain:

- The right to file an ECOA complaint for intentional discrimination (disparate treatment). The bar is higher but it’s still law.

- Adverse action notice requirements. Under ECOA, lenders must still tell you why you were denied. Demand written adverse action notices for every denial.

- Section 1071 data access (starting 2028). When available, lending data will be public. It will be thinner than originally mandated, but it will exist.

- Private right of action under ECOA. You can still sue. The legal theory just narrowed — you need intent, not impact.

- Fair Housing Act claims for mortgage discrimination — disparate impact still applies here.

Step 6: Connect With Advocacy Organizations

The organizations challenging the Regulation B rule change are also building the support infrastructure for women affected by it:

- National Fair Housing Alliance — leading the legal challenge. Read about the NFHA legal counter-offensive.

- National Women’s Business Council — tracks policy changes affecting women-owned businesses

- SBA Office of Advocacy — accepts public comment on rules affecting small businesses

- Your state’s women’s business center — SBA-funded centers in every state provide lending guidance

The Bigger Picture: Why Federal Protection Mattered

State-level protection is better than nothing. It is not better than a functioning federal standard.

The Equalizer Problem

Federal disparate impact was the closest thing women business owners had to an equalizer. It worked because it didn’t require proving what’s inside a loan officer’s head. It required data. It required showing the outcome. It forced lenders to justify policies that produced discriminatory results, regardless of stated intent.

The Dorsey analysis on the CFPB’s elimination proposal makes a key point: without disparate impact, enforcement shifts entirely to after-the-fact litigation by individual borrowers who must fund their own legal challenges. That’s not a system designed for a sole proprietor with $50,000 in revenue.

The Zip Code Lottery

After July 21, a woman applying for a business loan in New York has fundamentally different legal rights than a woman applying for the same loan in Texas. Not marginally different. Categorically different.

The New York applicant can challenge a policy that denies women at twice the rate of men — using statistics alone. The Texas applicant cannot. She needs to prove the lender deliberately discriminated against her. Same loan product. Same bank. Different state. Different rights.

That’s not a policy disagreement. It’s a constitutional problem. Read why your zip code determines your lending rights for the full analysis.

The Multi-State Problem

If your business operates across state lines — and increasingly, whose doesn’t? — the patchwork creates genuine operational confusion:

- Which state’s law applies? Your state of incorporation? The lender’s state? The state where the transaction was processed?

- Which complaint portal do you use? If you’re incorporated in Delaware, headquartered in Georgia, and the lender is in California, three different state regimes potentially apply.

- Can you choose the strongest state? Sometimes. Online lending transactions may give you more flexibility in which state’s consumer protection framework covers the relationship. But this is untested legal territory.

Federal law eliminated this confusion. One standard. One enforcement body. One complaint form. That infrastructure is gone.

Who’s Fighting Back

The July 21 rule is not going unchallenged. Know who’s in the fight:

- National Fair Housing Alliance filed a federal lawsuit on May 27, 2026 to block the rule. Read about the NFHA legal counter-offensive.

- Rise Economy, BLDS, and SolasAI are co-plaintiffs in the federal challenge.

- State AG coalitions are preparing independent enforcement frameworks to fill the federal gap.

- Consumer advocacy groups including the National Consumer Law Center are developing litigation toolkits for individual borrowers.

- Congressional allies have introduced legislation to codify disparate impact under ECOA — though passage in the current Congress is unlikely.

The legal challenge is real. The arguments are strong. But the timeline is tight — and operating as if the injunction will save you is not a strategy. It’s a wish.

FAQ: State Lending Protections After July 21

Q: Does my state’s fair lending law protect me if the lender is based in another state?

Generally, the law of the state where the lending transaction occurs applies — which typically means either where the borrower is located or where the lender is chartered, depending on jurisdiction. Online lending complicates this. If you’re in a Tier 1 state, your state’s law likely covers you regardless of where the lender is headquartered. If you’re in a Tier 3 state borrowing from a Tier 1-chartered lender, you may have an argument for applying the lender’s home state standard — but it’s untested.

Q: Can I relocate my business to get stronger protections?

You don’t need to relocate. What matters is where the lending transaction occurs — and, increasingly, where the lender is chartered. A more practical strategy: choose lenders headquartered in Tier 1 states, which often apply their home state’s higher compliance standards nationally.

Q: Is the July 21 date final?

The rule is published and the effective date is set. The only thing that changes it is a court injunction from the NFHA lawsuit or a new rulemaking — neither guaranteed. Plan as if July 21 is final.

Q: What about credit unions?

Credit unions are covered by ECOA and most state fair lending statutes. Federally chartered credit unions are regulated by the NCUA, not the CFPB. State-chartered credit unions in Tier 1 states are subject to the full state fair lending framework.

Q: What if I already filed a disparate impact complaint?

Consult an attorney immediately. Transition provisions may affect pending claims differently than new ones. Don’t assume your existing case automatically survives the rule change.

The Bottom Line

Federal disparate impact was a shield. It wasn’t perfect, but it was the one tool that didn’t require you to read a loan officer’s mind to prove discrimination. After July 21, that shield disappears at the federal level.

What replaces it depends entirely on where you live.

If you’re in New York, California, Massachusetts, Illinois, or Washington, your state built its own version. Use it. If you’re in a Tier 3 state, your options narrowed dramatically — but they didn’t disappear entirely. Strategic lender selection, meticulous documentation, and aggressive use of AG complaint channels still matter.

The six federal safeguards disappearing this year represent the most significant rollback of lending discrimination protections in decades. The state map is the new terrain. Know it. Use it. And stop waiting for Washington to have your back — because it’s already turned around.

Related: The Disparate Impact Countdown · The Protection Collapse Map · The 2026 Funding Gap Data

HerCapital covers the capital strategies, funding systems, and financial infrastructure that determine which women-owned businesses grow and which get stuck. No fluff, no cheerleading — just the information the funding industry isn’t volunteering.